On this page

- What Are Options Greeks?

- DELTA — Questions and Answers

- What Is Delta in Options?

- What Are the Delta Values for Different Options?

- Is Delta Different for Call and Put Options?

- Can You Show a Real Delta Example for Nifty?

- Does Delta Also Tell You Probability?

- What Happens to Delta When You Sell an Option?

- THETA — Questions and Answers

- What Is Theta in Options?

- How Much Does Theta Decay Per Day?

- Can You Show a Real Theta Example Using Nifty Weekly Options?

- Is Theta Always Bad?

- What Is the Weekend Theta Trap?

- GAMMA — Questions and Answers

- What Is Gamma in Options?

- Why Is Gamma Called the "Hidden Accelerator"?

- Is Gamma Good or Bad?

- What Is Special About Gamma on Expiry Day?

- VEGA — Questions and Answers

- What Is Vega in Options?

- Can You Show a Real Vega Example?

- What Is IV Crush, and Why Is It the Trap Beginners Fall Into?

- When Should You Buy or Sell Options Based on Vega?

- How Do All Four Greeks Work Together?

- And for Option Sellers?

- Quick Cheat Sheet: Greeks at a Glance

- How to Check Greeks Before Placing a Trade (Using Sensibull)

- Five Golden Rules From the Greeks

- FAQ

- Conclusion

- Ready to Put Greeks Into Practice?

Options Greeks Explained: Delta, Theta, Gamma and Vega Guide

What are options Greeks? Learn Delta, Theta, Gamma and Vega explained simply with real Nifty examples for Indian traders. Q&A format guide.

Options ki duniya mein ek cheez hai jo most retail traders completely ignore karte hain — aur isi wajah se woh lose karte hain even when they are right about the market direction.

Those things are Options Greeks.

Greeks tell you exactly how and why your option premium changes. Bina Greeks samjhe, aap essentially ek car drive kar rahe ho bina speedometer, fuel gauge, ya dashboard dekhe. You are moving, but you have no idea how fast, how much fuel is left, or when you will break down.

This guide answers every important question about Options Greeks in simple, plain language — specifically for Indian traders on NSE. No complex math, no confusing formulas — just real examples using Nifty so you can actually apply this the next time you are about to place a trade.

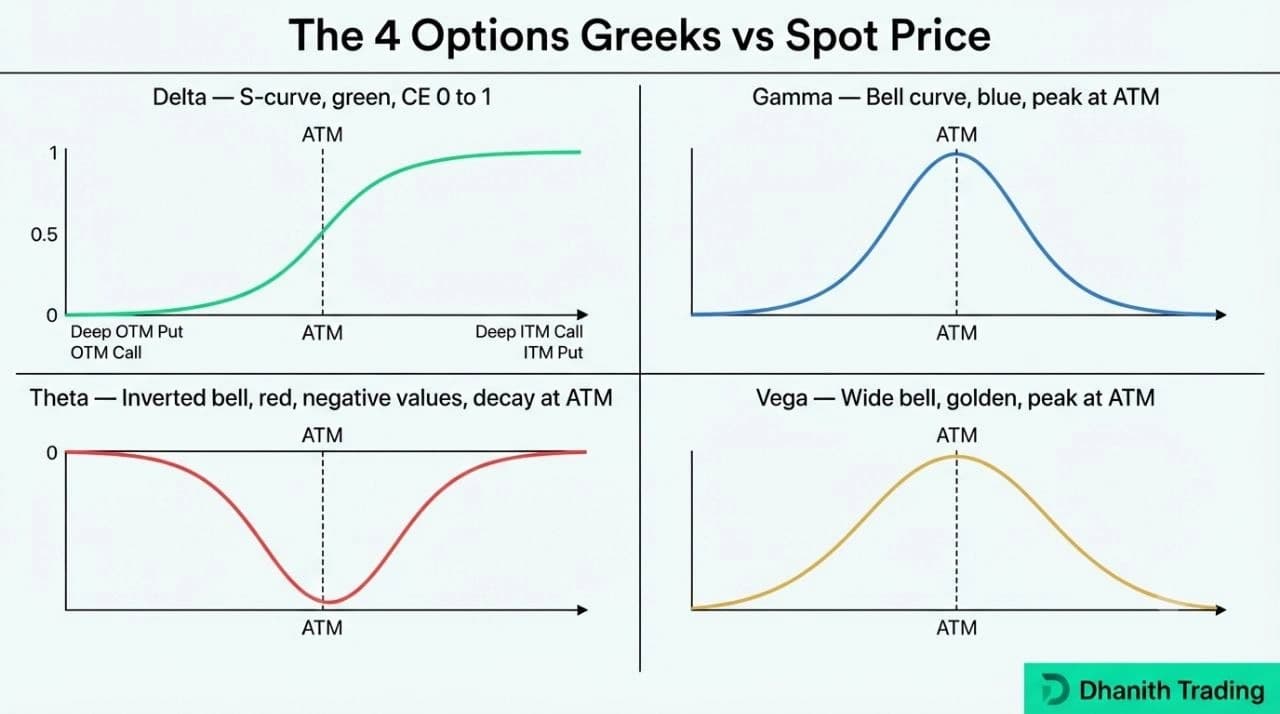

What Are Options Greeks?

Options Greeks are a set of measurements that tell you how sensitive your option premium is to specific factors — market movement, time passing, volatility, and more.

Think of them exactly like a car dashboard:

DELTA → Speedometer (how fast your premium moves)

THETA → Fuel gauge (how much premium burns every day)

VEGA → Weather sensor (how sensitive you are to storms/volatility)

GAMMA → Accelerator (how fast Delta itself is changing)

There are four primary Greeks every options trader must understand: Delta, Theta, Gamma, and Vega. Each one measures a different type of risk and reward, and together they explain almost everything that happens to your option price.

DELTA — Questions and Answers

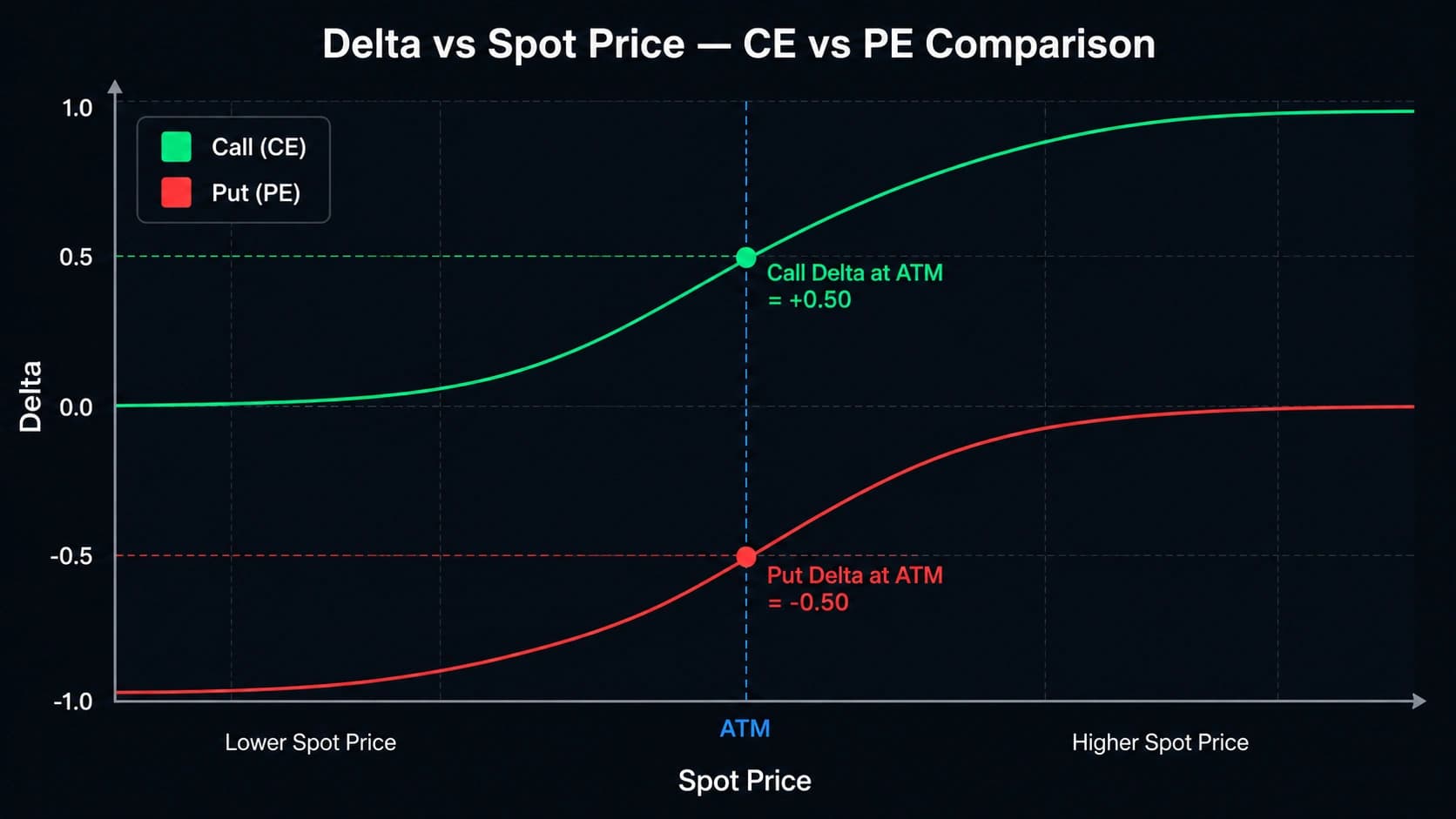

What Is Delta in Options?

Delta measures how much your option premium changes for every ₹1 move in the underlying stock or index.

If your option has a Delta of 0.5, and Nifty moves up by ₹100, your option premium will increase by approximately ₹50. Simple as that.

What Are the Delta Values for Different Options?

Deep ITM option → Delta near 1.0 (moves almost 1:1 with Nifty)

ATM option → Delta near 0.5 (moves ₹0.5 per ₹1 Nifty move)

OTM option → Delta near 0.2 (barely reacts to market moves)

Deep OTM option → Delta near 0.05 (almost does not move at all)

This is a critical number to check before buying any option. If you are buying a deep OTM option with a Delta of 0.05, even a 200-point Nifty move in your direction will only move your premium by ₹10. Is that worth the premium you paid? Usually not.

Is Delta Different for Call and Put Options?

Yes — Delta has a positive sign for Calls and a negative sign for Puts.

| Option Type | Delta Sign | What It Means |

|---|---|---|

| Call (CE) | Positive (+) | Premium goes UP when market rises |

| Put (PE) | Negative (-) | Premium goes UP when market falls |

This is intuitive: a CE is a bullish bet, so it benefits when the market goes up. A PE is a bearish bet, so it benefits when the market goes down.

Can You Show a Real Delta Example for Nifty?

Absolutely. Here is a complete, step-by-step example:

Nifty is at 24,000

You buy the 24,000 CE (ATM) — Delta = 0.5 — Current Premium = ₹100

Scenario 1: Nifty moves UP by ₹100 (to 24,100)

Premium change = 0.5 × 100 = +₹50

New premium = ₹150 — Profit: ₹50 per unit

Scenario 2: Nifty moves DOWN by ₹100 (to 23,900)

Premium change = 0.5 × (-100) = -₹50

New premium = ₹50 — Loss: ₹50 per unit

Since Nifty lot size is 75 units, every ₹50 premium change equals ₹3,750 on one lot.

Does Delta Also Tell You Probability?

Yes — Delta doubles as a rough probability indicator.

Delta approximately equals the probability that the option will expire In The Money.

- ATM CE with Delta 0.5 → roughly 50% chance of expiring ITM

- OTM CE with Delta 0.2 → roughly 20% chance of expiring ITM

- Deep OTM CE with Delta 0.05 → roughly 5% chance of expiring ITM

This is exactly why deep OTM cheap options are often called "lottery tickets" — you are paying for a low-probability bet. The premium looks small, but the probability of actually making money is also very small.

What Happens to Delta When You Sell an Option?

When you sell an option, your Delta works in reverse.

- You sell 24,000 CE → Your effective Delta = -0.5

- Nifty goes UP ₹100 → You lose ₹50 per unit

- Nifty goes DOWN ₹100 → You gain ₹50 per unit

As a seller, you want the market to stay flat or move against the option direction — because you are on the other side of the buyer's bet.

THETA — Questions and Answers

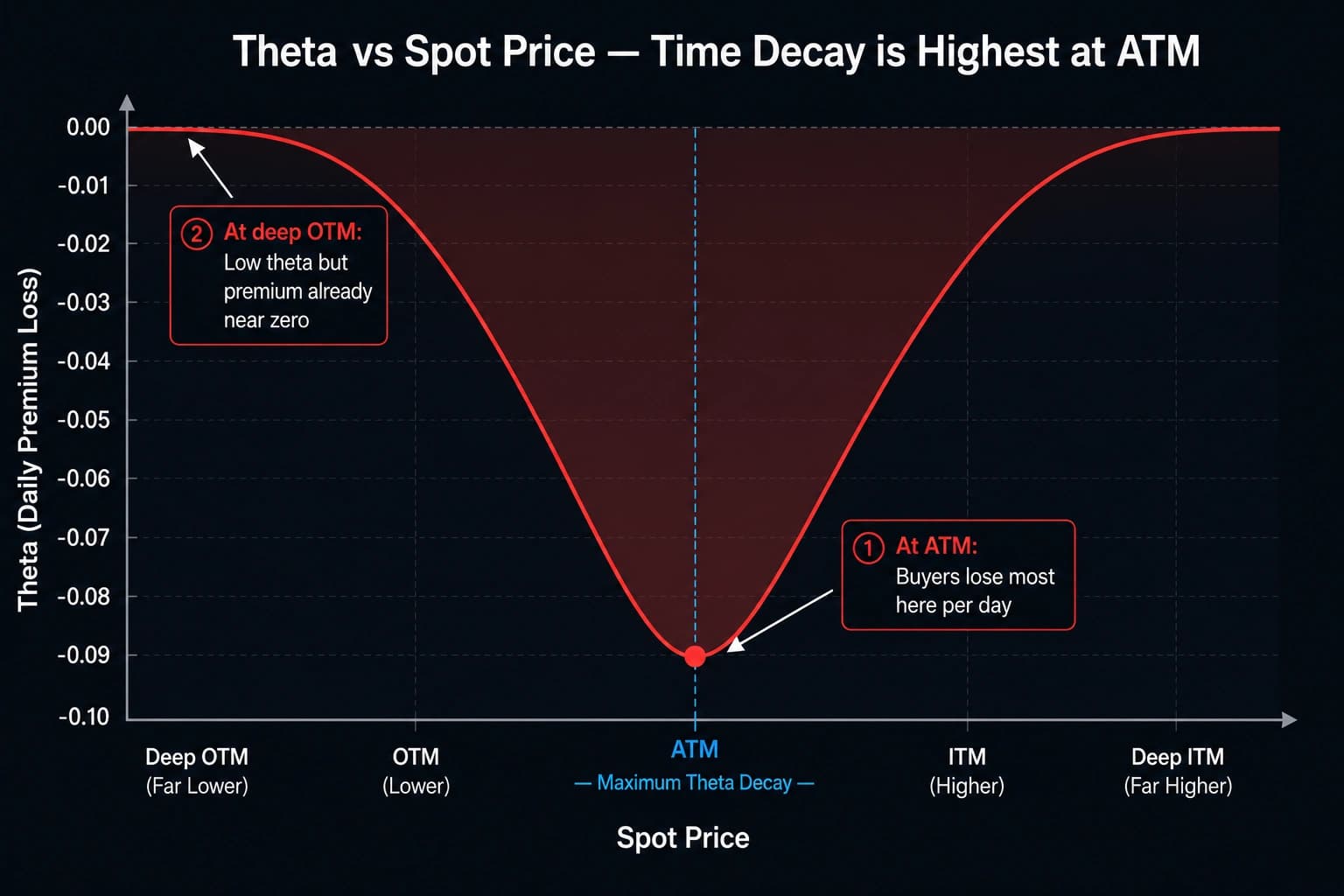

What Is Theta in Options?

Theta is the amount of premium your option loses every single day — even if the market does not move at all.

This is the single most important Greek for beginners to deeply understand, because it is the single biggest reason option buyers lose money even when they are right about direction. If you hold an option and the market stays flat, Theta is silently draining its value every single day.

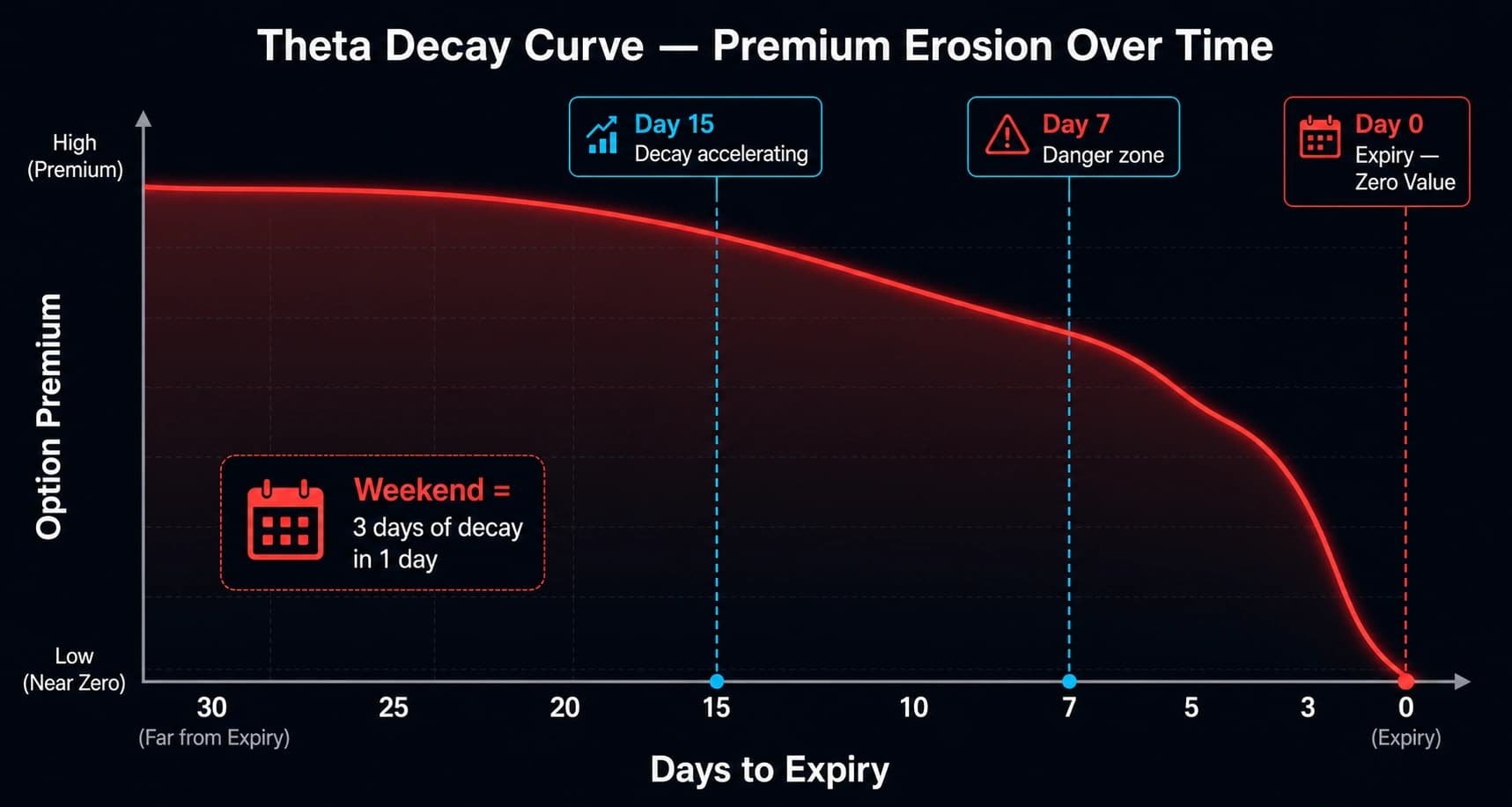

How Much Does Theta Decay Per Day?

Theta decay is not constant — it accelerates dramatically as expiry approaches.

30 days to expiry → Slow decay (~₹5-10 per day)

15 days to expiry → Medium decay (~₹15-20 per day)

7 days to expiry → Fast decay (~₹30-40 per day)

3 days to expiry → Very fast (~₹50-70 per day)

Expiry day itself → Brutal (premium collapses to zero by 3:30 PM)

The decay curve looks like this:

Premium

| \

| \

| \___

| \____

| \______

|_________________________

30 days 15 days Expiry

Gentle at first. Then increasingly steep. Then a cliff in the final days.

Can You Show a Real Theta Example Using Nifty Weekly Options?

Yes — and this example is exactly what most beginners experience without realizing what is happening to them.

Thursday 9:15 AM (new week's contract)

You buy Nifty 24,000 CE (weekly expiry: next Tuesday)

Premium paid = ₹100

Total investment = ₹100 × 75 = ₹7,500

Friday — Nifty still at 24,000, has not moved

Theta decay = ₹15

New premium = ₹85 — Position value = ₹6,375

Loss so far = ₹1,125 (Theta did this, not market direction)

Monday — Nifty still has not moved

Theta decay = ₹25 (accelerating)

New premium = ₹60 — Position value = ₹4,500

Loss so far = ₹3,000

Tuesday 9:15 AM — Nifty still at 24,000

Premium = ₹25 and falling rapidly toward zero by 3:30 PM

You lost ₹5,625 over four days — even though Nifty never moved against you. This is the Theta trap, and it catches thousands of beginners every week on NSE.

Is Theta Always Bad?

Only for buyers. For sellers, Theta is their best friend.

When you sell an option, every day that passes works in your favor — the premium you collected slowly erodes toward zero, and you keep the difference.

You sell the 24,000 CE for ₹100 premium

Every day Nifty stays below 24,000 → premium decays

By Tuesday (expiry) → Premium = ₹0 → You keep the full ₹7,500

This is why most professional traders lean toward being net option sellers — Theta is always on their side.

What Is the Weekend Theta Trap?

Friday ke baad 3-day weekend hota hai — aur market band rahta hai, lekin option premium Monday ko 3 dino ki decay ke saath open hota hai.

If you buy an option on Friday expecting a gap-up on Monday, you are paying for three days of Theta loss in a single weekend. This is exactly why many experienced traders avoid holding option buys over long weekends.

GAMMA — Questions and Answers

What Is Gamma in Options?

Gamma tells you how fast Delta itself is changing as the underlying moves.

Delta is not a fixed number — it moves as Nifty moves. Gamma measures the speed of that movement.

Nifty @ 24,000

You hold 24,000 CE: Delta = 0.50, Gamma = 0.003

Nifty moves UP ₹100 → New Delta = 0.50 + (0.003 × 100) = 0.80

Nifty moves UP another ₹100 → New Delta = 0.80 + 0.30 = 1.0

Your option Delta went from 0.50 to 1.0 as Nifty moved up 200 points. The option is accelerating — gaining value faster with each passing point.

Why Is Gamma Called the "Hidden Accelerator"?

Because Gamma is what turns a moderate Nifty move into a 5x or 10x return on an ATM option. When a big, fast move happens, Delta accelerates through Gamma, which means the option value starts compounding upward much faster than the simple Delta calculation alone would suggest.

This is why ATM options on genuinely large-move days can produce outsized returns even on what looks like a modest point move.

Is Gamma Good or Bad?

It completely depends on whether you are a buyer or a seller.

| Option Buyer | Option Seller | |

|---|---|---|

| Gamma Sign | Positive (your friend) | Negative (your enemy) |

| When a big move happens | Delta accelerates — Profits grow fast | Delta accelerates — Losses grow fast |

| When nothing moves | Theta quietly kills you | Theta quietly pays you |

As a buyer: Gamma is what gives you the possibility of outsized wins, but Theta is simultaneously draining the premium while you wait.

As a seller: Gamma is your biggest risk — a large, sudden market move causes your short option Delta to rapidly accelerate against you.

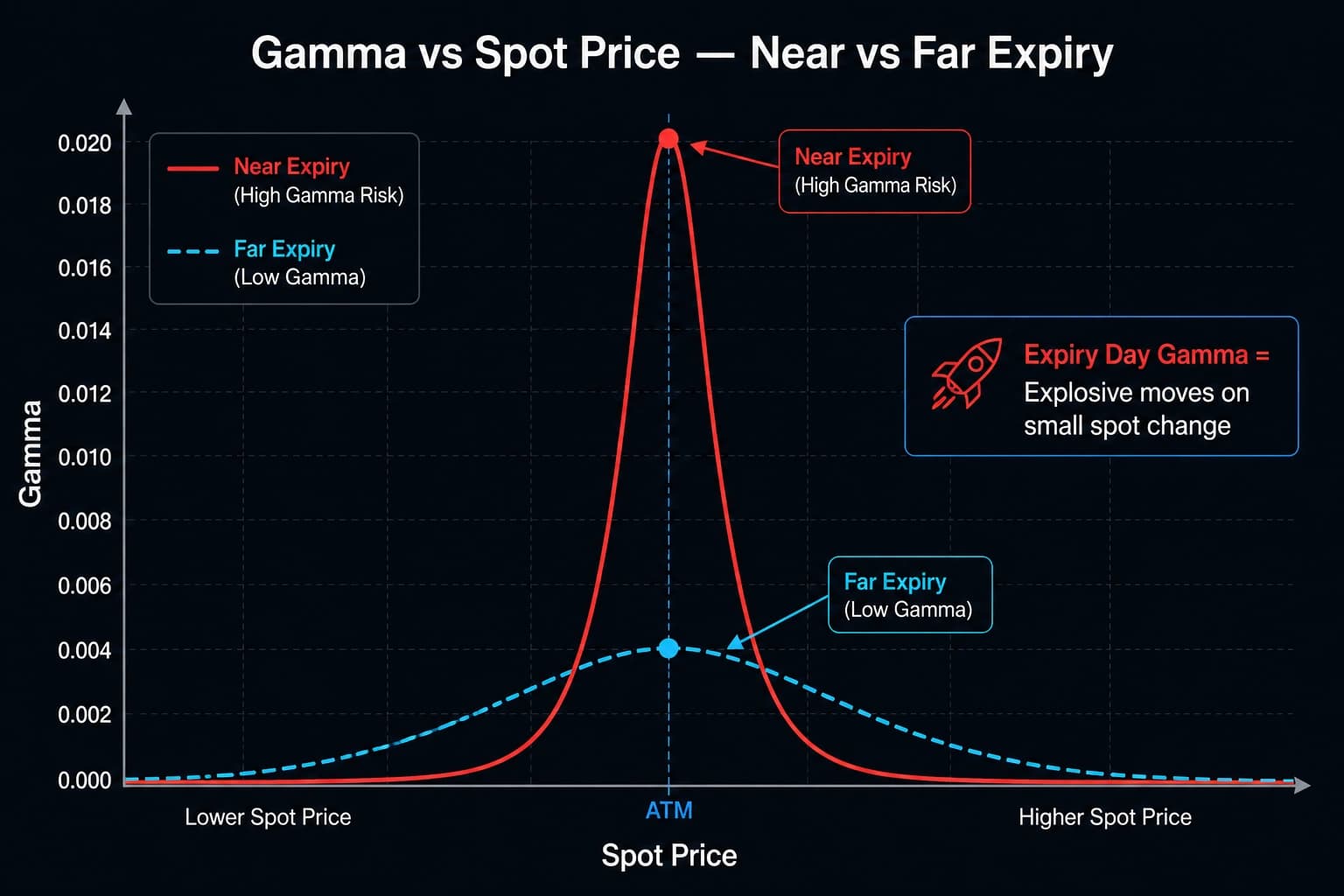

What Is Special About Gamma on Expiry Day?

Expiry day has the highest Gamma of any day in the option life.

This is why expiry day is simultaneously the day of greatest opportunity and greatest danger.

On expiry day:

A 50-point Nifty move can cause 200-400% premium change on ATM options

A trader positioned correctly can see extraordinary percentage returns. A seller caught in an unexpected move can face devastating losses — in the same session.

VEGA — Questions and Answers

What Is Vega in Options?

Vega measures how much your option premium changes for every 1% change in Implied Volatility (IV).

Implied Volatility is how much movement the market is expecting in the near future, and it can rise or fall completely independently of whether Nifty itself actually moves. This catches most beginners completely off-guard.

IV goes UP → All option premiums go UP (good for buyers)

IV goes DOWN → All option premiums go DOWN (bad for buyers)

Can You Show a Real Vega Example?

Nifty 24,000 CE premium = ₹100

Current IV = 15%, Vega = 0.8

Scenario: RBI policy announcement tomorrow — IV spikes to 20% (+5%)

Premium change = 0.8 × 5 = +₹4 per 1% rise — Total +₹20

New premium = ₹120 (even if Nifty has not moved at all)

Scenario: Event passes quietly — IV falls to 12% (-3%)

Premium change = 0.8 × (-3) = -₹2.4 per 1% — Total -₹7.2

New premium = ₹92.8

Notice: even if Nifty moved where you expected, IV falling after the event erodes a meaningful chunk of your gain.

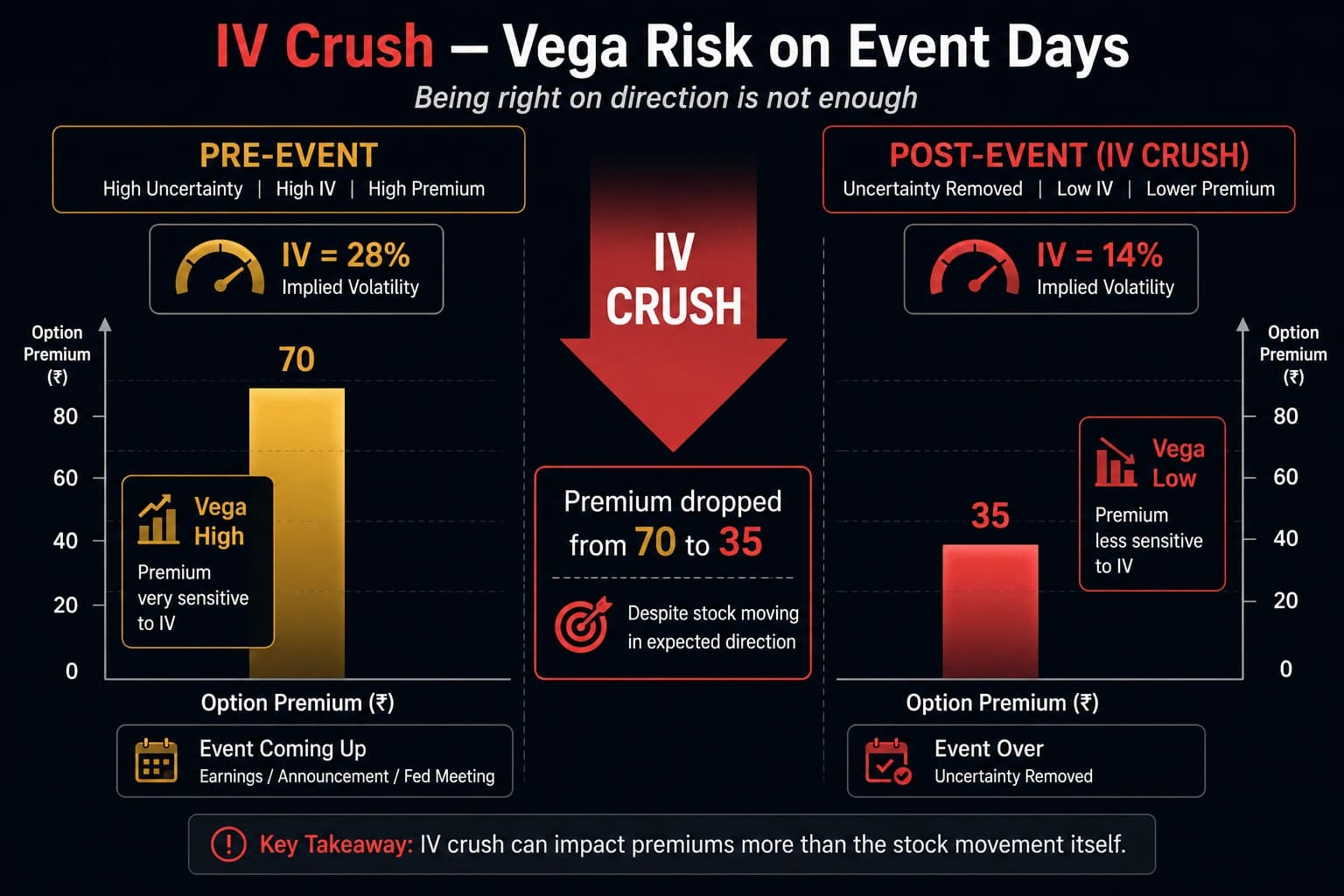

What Is IV Crush, and Why Is It the Trap Beginners Fall Into?

IV Crush is when Implied Volatility falls sharply after a big event, taking option premiums down with it — even if the market moved in your predicted direction.

Before Budget Day — IV = 22% (everyone expects a big move, premiums inflated)

You buy a CE for ₹150

Budget announced — Nifty moves UP 200 points as you expected!

But IV crashes to 14% after the event (uncertainty gone, market calmed)

Delta gain from 200-point move = +₹100

IV Crush loss from IV falling = -₹64

Net premium = ₹186 (only ₹36 profit despite being right about direction)

You were RIGHT about the market. You still barely made any money. This is one of the most consistently observed, most painful experiences for beginner options traders. Being directionally correct is not enough — you also need to understand volatility timing.

When Should You Buy or Sell Options Based on Vega?

| Situation | What Happens to IV | Best Action |

|---|---|---|

| Before a big event (Budget, RBI, Results) | IV is high, premiums inflated | Sell options — collect inflated premium |

| After the event passes | IV crashes (IV Crush) | Buyers get hurt; sellers benefit |

| Market is calm, VIX is low | IV is low, premiums are cheap | Buy options — Vega works for you if IV rises later |

| VIX spikes suddenly | Fear building, IV rising | Options getting expensive fast |

How Do All Four Greeks Work Together?

Understanding each Greek individually is useful. But in a real trade, all four are affecting your premium simultaneously. Here is how they combine when you buy an ATM option on a Monday morning:

Greek Effect on Your Position Friend or Enemy?

-------------------------------------------------------

Delta +0.5 (need market to move up) Friend if market rises

Theta -₹20 per day ENEMY — always draining

Gamma +0.003 Friend if a big move happens

Vega +0.8 (need IV to stay up) Enemy if IV falls after entry

To profit as an option buyer, you need all of the following:

- ✓ Market moves in your direction (Delta)

- ✓ Market moves fast before Theta kills your premium (Theta)

- ✓ IV does not fall after you enter (Vega)

- ✓ The move is big enough that Gamma accelerates your gains

This is exactly why buying options is genuinely hard — you can be right about direction and still lose money if timing or volatility does not cooperate.

And for Option Sellers?

As a seller, the same four Greeks flip to work mostly in your favor:

- ✓ Theta pays you every single day

- ✓ IV falling benefits you through Vega

- ✓ You only need the market to stay within a range

- ✗ One genuinely large, unexpected move turns Gamma into your enemy

Quick Cheat Sheet: Greeks at a Glance

| Greek | What It Measures | Buyer Gets | Seller Gets |

|---|---|---|---|

| Delta | Direction sensitivity | + for CE, - for PE | Opposite of buyer |

| Theta | Daily time decay | Always loses premium | Always gains premium |

| Gamma | How fast Delta changes | Accelerating gains on big moves | Accelerating losses on big moves |

| Vega | Volatility sensitivity | Gains if IV rises | Gains if IV falls |

How to Check Greeks Before Placing a Trade (Using Sensibull)

Before placing any options trade, follow these six steps on Sensibull (free tool):

Step 1 → Select your strike (e.g. Nifty 24,000 CE)

Step 2 → Check Delta — Is it between 0.3 and 0.6? (ATM zone, safer for buyers)

Step 3 → Check Theta — How much premium am I losing per day?

Step 4 → Check IV — Is current IV high or low vs historical average?

Step 5 → Check days to expiry — More days remaining = slower Theta decay

Step 6 → Only enter if the risk/reward after Greeks actually makes sense

Most beginners skip straight to Step 6. That is exactly what changes once you understand Greeks — you will automatically check Steps 2 through 5 before every single trade.

Five Golden Rules From the Greeks

-

Never buy OTM options on expiry day. Theta plus high Gamma equals 100% loss if the market does not move immediately and significantly in your direction.

-

Buy options when IV is LOW. You want Vega working for you — cheap premiums mean IV has room to rise after you enter.

-

Sell options when IV is HIGH. Both Theta and Vega work in your favor — you collect inflated premium and benefit from IV returning to normal.

-

Respect the weekend Theta trap. Friday mein open position leke jaoge to 3 dino ka decay Monday ko ek saath milega. Always account for this.

-

Buy ATM options only when you genuinely expect a big move. Gamma accelerates your gains on large moves — but Theta destroys you if the move does not materialize fast enough.

FAQ

Q: What is Delta in options trading? Delta measures how much an option premium changes for every ₹1 move in the underlying stock or index. An ATM option typically has a Delta of 0.5, meaning the premium moves ₹0.5 for every ₹1 Nifty move. Delta also roughly indicates the probability of an option expiring In The Money.

Q: What is Theta in options, and why is it dangerous for buyers? Theta is the daily time decay of an option premium — the amount your option loses in value every single day, even if the market does not move at all. Theta accelerates significantly as expiry approaches, which is why holding a Nifty weekly option from Thursday to Tuesday without a favorable market move can result in large losses purely from time passing.

Q: What is Gamma in options? Gamma measures how fast an option Delta changes as the underlying moves. High Gamma means Delta is changing rapidly — which benefits buyers during large, fast moves but creates accelerating risk for sellers in the same scenario. Gamma is at its highest on expiry day, making ATM options extremely sensitive to even small market moves.

Q: What is Vega in options, and what is IV Crush? Vega measures how much an option premium changes for every 1% change in Implied Volatility. IV Crush happens when IV falls sharply after a major event like a Budget or RBI policy, collapsing option premiums even if the market moved in the direction you predicted. This is one of the most common reasons beginners lose money even when they are right about market direction.

Q: Should you buy or sell options based on IV levels? When IV is low and premiums are cheap, buying options gives Vega the chance to work in your favor if volatility rises later. When IV is high before a big event and premiums are inflated, selling options lets you collect elevated premium and benefit from IV returning to normal levels after the event passes.

Q: How do I check Greeks before placing an options trade? Use free tools like Sensibull or Opstra. Select your intended strike, then check Delta (is it in the ATM range of 0.3 to 0.6?), Theta (how much am I losing per day?), IV (is it currently high or low?), and days to expiry (how much time do I have before decay accelerates?). Only enter if the Greeks collectively support a favorable risk-reward for your specific trade plan.

Conclusion

Understanding Options Greeks separates traders who actually know what is happening to their positions from those who are guessing and hoping. The difference between a beginner who buys a Nifty CE before a Budget and loses money despite being right about direction — and the trader on the other side who knew IV Crush was coming — is exactly this knowledge.

Delta, Theta, Gamma, and Vega are not abstract academic concepts. They are the four forces acting on your option premium in real time, every single trading day. Once checking them before a trade becomes instinctive, your decision-making will improve more than any new strategy or screener ever could.

Start with Theta. It is the most important Greek for most retail buyers to understand first, because it is the one that quietly, invisibly destroys more trading accounts than any wrong directional call ever has.

Further reading: What Is Options Trading? A Complete Beginner's Guide | How to Analyse Option Chain: Complete NSE Guide | Best Online Trading Journal: Why Serious Traders Track Every Trade

Ready to Put Greeks Into Practice?

→ Log Every Options Trade in the Dhanith Journal — track which Greek conditions were present when you entered, and review whether they played out as expected

→ Calculate Your Risk Before Every Trade — know your exact lot cost and maximum loss before Theta starts working against you

Disclaimer: This blog is for educational purposes only and is not investment advice. Options trading involves substantial risk, and more than 90% of retail F&O traders lose money, as per a SEBI study. Always paper trade first, use only risk capital, and never trade without a defined exit plan.

Was this article helpful?

Click to rate

Trader & Founder, Dhanith Trading

Full-time trader focused on price action, Smart Money Concepts, and intraday strategies for Indian markets. Founder of Dhanith — a trading journal, intraday screener, and risk tools platform built for retail traders.

Dhanith Newsletter

Enjoyed this article? Get more like it.

New trading guides, candlestick patterns, SMC strategies, and tool updates — straight to your inbox. Free, for Indian traders.

No spam. Unsubscribe anytime.

Continue Reading